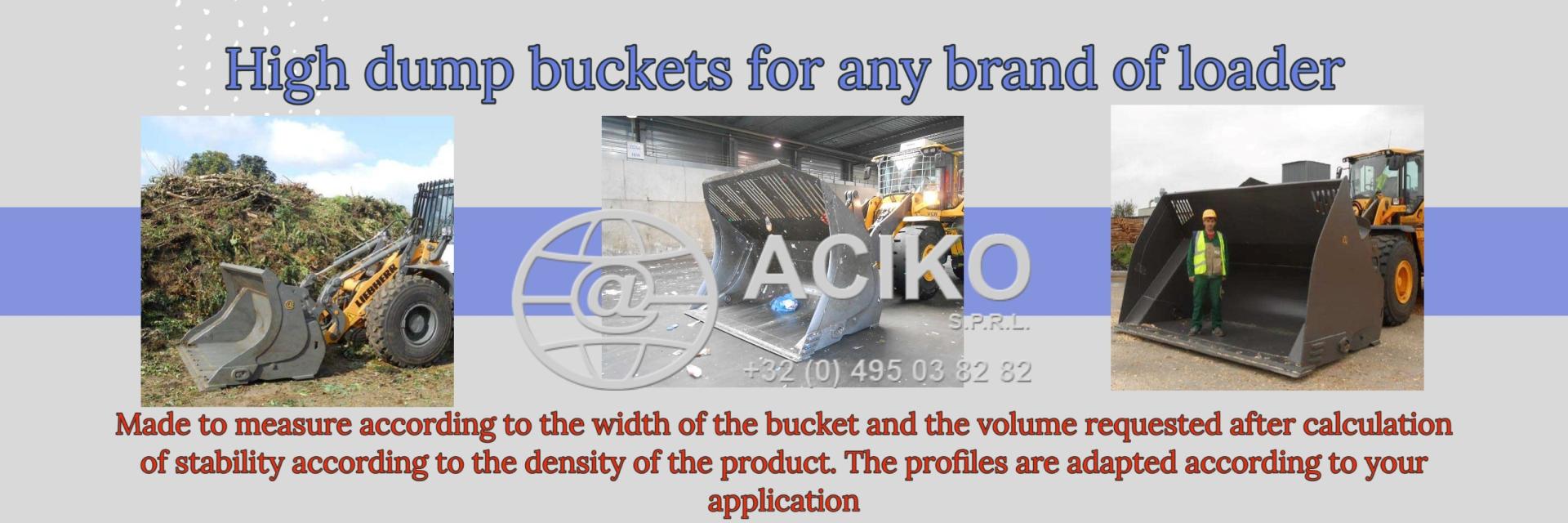

R.E.News International-CECE, CEMA and UNIDROIT call for adoption of the MAC Protocol to boost equipment financing in Europe

06/03/25-FR-English-NL-footer

06/03/25-FR-English-NL-footer

La CECE, la CEMA et UNIDROIT appellent à l'adoption du Protocole MAC pour stimuler le financement des équipements en Europe

IMAGE SOURCE: CECE

IMAGE SOURCE: CECE

La CECE, la CEMA et UNIDROIT plaident en faveur de l'adoption du Protocole MAC pour améliorer le financement des équipements en Europe.

Le Protocole MAC vise à créer un cadre juridique international commun, réduisant les risques financiers et améliorant les conditions de prêt pour les machines de grande valeur.

Le président de la CECE, José Antonio Nieto, a souligné le potentiel du protocole pour renforcer la sécurité juridique et soutenir les investissements dans les secteurs de la construction, de l'agriculture et des mines.

Le secrétaire général de la CEMA, Jelte Wiersma, a souligné les avantages du protocole pour les agriculteurs, rendant le financement plus accessible et prévisible pour les machines modernes et efficaces.

Le secrétaire général d'UNIDROIT, Ignacio Tirado, a souligné l'importance de la coopération internationale dans l'élaboration du Protocole MAC pour garantir le financement transfrontalier.

L'événement a souligné la nécessité pour les gouvernements européens et les acteurs de l'industrie de ratifier le Protocole MAC pour stimuler la croissance économique et la compétitivité.

Les leaders européens de l'industrie de la construction, de l'agriculture et du secteur juridique se sont réunis hier à Bruxelles pour discuter des avantages du Protocole sur les mines, l'agriculture et la construction (MAC) et de son potentiel pour améliorer le financement des équipements en Europe et dans le monde.

L'événement, organisé conjointement par le Comité européen des équipements de construction (CECE), l'Association européenne des machines agricoles (CEMA) et l'Institut international pour l'unification du droit privé (UNIDROIT), s'est concentré sur la manière dont le Protocole MAC peut faciliter un accès plus facile et plus sûr au crédit lors d'investissements dans des machines de grande valeur. En créant un cadre juridique international commun, le protocole contribuera à réduire les risques financiers et à améliorer les conditions de prêt, en particulier pour les petites et moyennes entreprises.

Le président de la CECE, José Antonio Nieto, a qualifié le protocole MAC d'avancée majeure pour les industries représentées, déclarant : « Le protocole MAC est un changement radical pour nos secteurs. Il est conçu pour améliorer la sécurité juridique, faciliter l'accès au crédit et soutenir l'investissement dans des équipements de grande valeur, notamment les machines utilisées dans la construction, l'agriculture et l'exploitation minière. Ces industries constituent l'épine dorsale du développement des infrastructures européennes, de la sécurité alimentaire et de la gestion des ressources. En réduisant les risques financiers et en améliorant les options de financement basées sur les actifs, le protocole MAC ouvre de nouvelles portes aux entreprises de toutes tailles, en particulier aux PME, pour étendre leurs activités et investir dans l'innovation. »

Le secrétaire général de la CEMA, Jelte Wiersma, a souligné les avantages pour le secteur agricole, ajoutant : « Les agriculteurs ont besoin de machines modernes et efficaces pour rester compétitifs et atteindre les objectifs de durabilité, mais l'accès au financement peut être un véritable obstacle. Le protocole MAC peut contribuer à changer cela en rendant le financement plus accessible et prévisible. Cela permettra à davantage d'agriculteurs d'investir dans l'équipement dont ils ont besoin pour produire des aliments de manière efficace et durable. »

Le Secrétaire général d'UNIDROIT, Ignacio Tirado, a souligné l'impact considérable du protocole et l'importance de la coopération internationale pour le concrétiser : « Le Protocole MAC a été élaboré au cours d'années de collaboration entre experts juridiques, représentants de l'industrie et gouvernements. Il offre un cadre clair et efficace pour le financement d'équipements transfrontaliers, la réduction des coûts et la création d'un environnement plus sûr pour les prêteurs et les entreprises. »

Tout au long de l'événement, les intervenants et les participants ont discuté des avantages pratiques du Protocole MAC, de ce que son adoption signifierait pour les industries européennes et des prochaines étapes nécessaires à sa mise en œuvre aux niveaux national et européen. Il a été largement reconnu que l'entrée en vigueur du protocole renforcerait les fabricants européens, améliorerait les conditions de financement et soutiendrait les investissements à long terme dans l'innovation et la durabilité.

La CECE, la CEMA et UNIDROIT appellent les gouvernements européens et les acteurs de l'industrie à aller de l'avant avec la ratification du Protocole MAC, reconnaissant son potentiel pour stimuler la croissance économique et la compétitivité dans les secteurs industriels clés.

NJC.© Info CECE

--------------------------------------------------------------------------------------------------------------

06/03/25-English

CECE, CEMA and UNIDROIT call for adoption of the MAC Protocol to boost equipment financing in Europe

IMAGE SOURCE: CECE

CECE, CEMA, and UNIDROIT advocate for the adoption of the MAC Protocol to enhance equipment financing in Europe.

The MAC Protocol aims to create a common international legal framework, reducing financial risks and improving lending conditions for high-value machinery.

CECE President Jose Antonio Nieto emphasized the protocol's potential to enhance legal certainty and support investment in construction, agriculture, and mining sectors.

CEMA Secretary General Jelte Wiersma highlighted the protocol's benefits for farmers, making financing more accessible and predictable for modern, efficient machinery.

UNIDROIT Secretary-General Ignacio Tirado stressed the importance of international cooperation in developing the MAC Protocol to secure cross-border financing.

The event underscored the need for European governments and industry stakeholders to ratify the MAC Protocol to boost economic growth and competitiveness.

European industry leaders from the construction, agriculture and legal sectors gathered in Brussels yesterday to discuss the benefits of the Mining, Agriculture, and Construction (MAC) Protocol and its potential to improve equipment financing across Europe and globally.

The event, co-organized by the Committee for European Construction Equipment (CECE), the European Agricultural Machinery Association (CEMA), and the International Institute for the Unification of Private Law (UNIDROIT), focused on how the MAC Protocol can facilitate an easier and safer access to credit when investing in high-value machinery. By creating a common international legal framework, the protocol will help reducing financial risks and improve lending conditions—particularly for small and medium-sized businesses.

CECE President Jose Antonio Nieto called the MAC Protocol a major step forward for the industries represented, stating: "The MAC Protocol is a game-changer for our sectors. It is designed to enhance legal certainty, facilitate access to credit, and support investment in high-value equipment, including machinery used in construction, agriculture, and mining. These industries form the backbone of European infrastructure development, food security, and resource management. By reducing financial risks and improving asset-based financing options, the MAC Protocol opens new doors for companies of all sizes—especially SMEs—to expand their operations and invest in innovation."

CEMA Secretary General Jelte Wiersma underlined the benefits for the agricultural sector, adding: "Farmers need modern, efficient machinery to stay competitive and meet sustainability goals, but access to financing can be a real hurdle. The MAC Protocol can help change that by making financing more accessible and predictable. This will allow more farmers to invest in the equipment they need to produce food efficiently and sustainably."

UNIDROIT Secretary-General Ignacio Tirado highlighted the broad impact of the protocol and the importance of international cooperation in making it a reality: "The MAC Protocol has been developed through years of collaboration between legal experts, industry representatives, and governments. It offers a clear and effective framework for financing equipment across borders, reducing costs, and creating a more secure environment for lenders and businesses alike."

Throughout the event, speakers and participants discussed the practical benefits of the MAC Protocol, what its adoption would mean for European industries and the next steps required for implementation at both the national and EU levels. There was broad agreement that bringing the protocol into force would strengthen European manufacturers, improve financing conditions, and support long-term investment in innovation and sustainability.

CECE, CEMA, and UNIDROIT are calling on European governments and industry stakeholders to move forward with ratifying the MAC Protocol, recognizing its potential to boost economic growth and competitiveness across key industrial sectors.

NJC.© Info CECE

-------------------------------------------------------------------------------------------------------------------

06/03/25-NL

CECE, CEMA en UNIDROIT pleiten voor de invoering van het MAC-protocol om de financiering van apparatuur in Europa te stimuleren

IMAGE SOURCE: CECE

CECE, CEMA en UNIDROIT pleiten voor de invoering van het MAC-protocol om de financiering van apparatuur in Europa te verbeteren.

Het MAC-protocol heeft als doel een gemeenschappelijk internationaal juridisch kader te creëren, financiële risico's te verminderen en de leenvoorwaarden voor hoogwaardige machines te verbeteren.

CECE-voorzitter Jose Antonio Nieto benadrukte het potentieel van het protocol om de rechtszekerheid te vergroten en investeringen in de bouw-, landbouw- en mijnbouwsector te ondersteunen.

CEMA-secretaris-generaal Jelte Wiersma benadrukte de voordelen van het protocol voor boeren, waardoor financiering toegankelijker en voorspelbaarder wordt voor moderne, efficiënte machines.

UNIDROIT-secretaris-generaal Ignacio Tirado benadrukte het belang van internationale samenwerking bij de ontwikkeling van het MAC-protocol om grensoverschrijdende financiering veilig te stellen.

Het evenement onderstreepte de noodzaak voor Europese regeringen en belanghebbenden in de industrie om het MAC-protocol te ratificeren om de economische groei en het concurrentievermogen te stimuleren.

Europese industrieleiders uit de bouw-, landbouw- en juridische sectoren kwamen gisteren in Brussel bijeen om de voordelen van het Mining, Agriculture, and Construction (MAC) Protocol te bespreken en het potentieel ervan om de financiering van apparatuur in heel Europa en wereldwijd te verbeteren.

Het evenement, mede georganiseerd door het Committee for European Construction Equipment (CECE), de European Agricultural Machinery Association (CEMA) en het International Institute for the Unification of Private Law (UNIDROIT), richtte zich op hoe het MAC Protocol een eenvoudigere en veiligere toegang tot krediet kan vergemakkelijken bij het investeren in hoogwaardige machines. Door een gemeenschappelijk internationaal juridisch kader te creëren, zal het protocol helpen financiële risico's te verminderen en leenvoorwaarden te verbeteren, met name voor kleine en middelgrote bedrijven.

CECE-voorzitter Jose Antonio Nieto noemde het MAC-protocol een belangrijke stap voorwaarts voor de vertegenwoordigde industrieën en verklaarde: "Het MAC-protocol is een game-changer voor onze sectoren. Het is ontworpen om de rechtszekerheid te verbeteren, de toegang tot krediet te vergemakkelijken en investeringen in hoogwaardige apparatuur te ondersteunen, waaronder machines die worden gebruikt in de bouw, landbouw en mijnbouw. Deze industrieën vormen de ruggengraat van de Europese infrastructuurontwikkeling, voedselzekerheid en hulpbronnenbeheer. Door financiële risico's te verminderen en op activa gebaseerde financieringsopties te verbeteren, opent het MAC-protocol nieuwe deuren voor bedrijven van alle omvang, met name het MKB, om hun activiteiten uit te breiden en te investeren in innovatie."

CEMA-secretaris-generaal Jelte Wiersma onderstreepte de voordelen voor de landbouwsector en voegde toe: "Boeren hebben moderne, efficiënte machines nodig om concurrerend te blijven en duurzaamheidsdoelen te halen, maar toegang tot financiering kan een echte hindernis zijn. Het MAC-protocol kan helpen dat te veranderen door financiering toegankelijker en voorspelbaarder te maken. Hierdoor kunnen meer boeren investeren in de apparatuur die ze nodig hebben om efficiënt en duurzaam voedsel te produceren."

Secretaris-generaal van UNIDROIT, Ignacio Tirado, benadrukte de brede impact van het protocol en het belang van internationale samenwerking om het te realiseren: "Het MAC-protocol is ontwikkeld door jarenlange samenwerking tussen juridische experts, vertegenwoordigers van de industrie en overheden. Het biedt een duidelijk en effectief kader voor de financiering van apparatuur over de grenzen heen, verlaagt de kosten en creëert een veiligere omgeving voor zowel kredietverstrekkers als bedrijven."

Tijdens het evenement bespraken sprekers en deelnemers de praktische voordelen van het MAC-protocol, wat de invoering ervan zou betekenen voor Europese industrieën en de volgende stappen die nodig zijn voor implementatie op zowel nationaal als EU-niveau. Er was brede overeenstemming dat het van kracht worden van het protocol Europese fabrikanten zou versterken, de financieringsvoorwaarden zou verbeteren en langetermijninvesteringen in innovatie en duurzaamheid zou ondersteunen.

CECE, CEMA en UNIDROIT roepen Europese overheden en belanghebbenden in de industrie op om door te gaan met het ratificeren van het MAC-protocol, waarbij het potentieel ervan wordt erkend om de economische groei en het concurrentievermogen in belangrijke industriële sectoren te stimuleren.

NJC.© Info CECE

-------------------------------------------------------------------------------------------------------------

Date de dernière mise à jour : 05/03/2025